JOURNAL OF NATURAL RESOURCES >

The theory, logic, and reform path of implementing the budget for natural resource assets owned by the whole people

Received date: 2024-06-10

Revised date: 2024-09-04

Online published: 2025-02-21

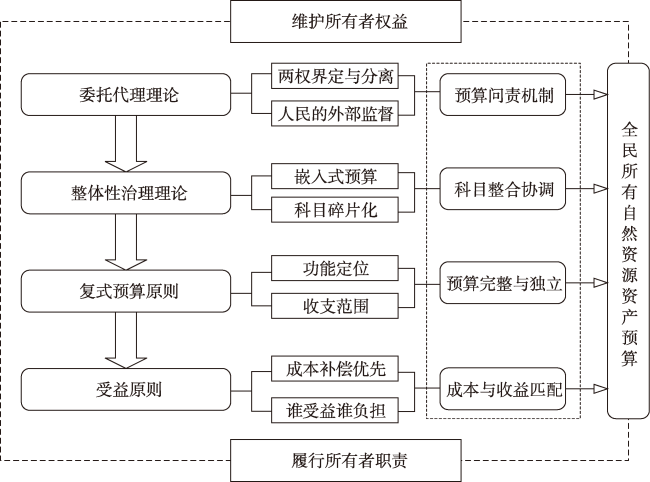

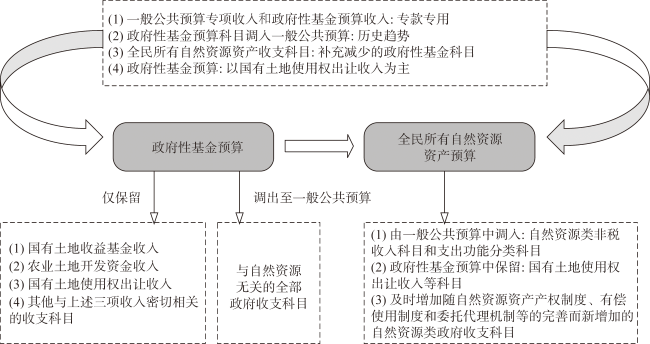

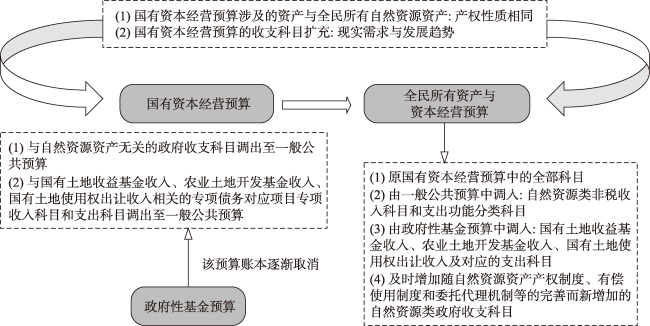

Revenue from natural resource assets owned by the whole people is an important part of national fiscal revenue, and strengthening budget management is of great significance in realizing the rights and interests and fulfilling the responsibilities of owners of natural resource assets owned by the whole people. Based on the logic of principal-agent theory, holistic governance theory, compound budget principle and benefit principle, this paper argues that the implementation of the budget for natural resource assets owned by the whole people is a necessary choice to promote the unification of the rights and responsibilities of natural resource asset owners. The implementation of the budget for natural resource assets owned by the whole people is not only conducive to optimizing the structure of fiscal revenue, realizing the central and local government fiscal rights and expenditure responsibilities in the field of natural resources, and dealing with the relationship between the government and the market, but also an important way to strengthen the overall function of the full-caliber budget and further improve the full-caliber budget management system. Under the background of the pilot commissioning mechanism for the ownership of natural resource assets owned by the whole people and the new round of reform of the fiscal and tax system, based on adjustments to the government revenue and expenditure classification accounts, this paper believes that the gradual transition from "government fund budget" to "budget for natural resource assets owned by the whole people" and the gradual transition from "state-owned capital operating budget" to "budget for assets and capital operations owned by the whole people" are the two alternative ways of implementing the budget for natural resource assets owned by the whole people. In addition, the implementation of the budget for natural resource assets owned by the whole people should focus on the four aspects of "value accounting, budget harmonization, planning and adjustment, and performance evaluation". This paper puts forward a prototype of the budget for natural resource assets owned by the whole people, which provides a reference for decision-making to improve the natural resource asset revenue management system and standardize government revenues and expenditures in the field of natural resources.

CHEN Xu-dong , LU Hong-yuan . The theory, logic, and reform path of implementing the budget for natural resource assets owned by the whole people[J]. JOURNAL OF NATURAL RESOURCES, 2025 , 40(3) : 618 -635 . DOI: 10.31497/zrzyxb.20250304

| [1] |

潘楚元, 苏时鹏. 国有自然资源资产管理: 功能定位、特征事实与国别比较借鉴. 自然资源学报, 2023, 38(7): 1682-1697.

[

|

| [2] |

郭韦杉, 李国平, 王文涛. 自然资源资产核算: 概念辨析及核算框架设计. 中国人口·资源与环境, 2021, 31(11): 11-19.

[

|

| [3] |

杨世忠, 谭振华, 王世杰. 论我国自然资源资产负债核算的方法逻辑及系统框架构建. 管理世界, 2020, 36(11): 132-144.

[

|

| [4] |

黄溶冰, 赵谦, 王丽艳. 自然资源资产离任审计与空气污染防治: “和谐锦标赛”还是“环保资格赛”. 中国工业经济, 2019, (10): 23-41.

[

|

| [5] |

钟廷勇, 许超亚, 孙芳城. 领导干部自然资源资产离任审计与企业社会责任履行. 财经问题研究, 2022, (12): 92-103.

[

|

| [6] |

郭贯成, 崔久富, 李学增. 全民所有自然资源资产“三权分置”产权体系研究: 基于委托代理理论的视角. 自然资源学报, 2021, 36(10): 2684-2693.

[

|

| [7] |

李鹏辉, 张茹倩, 徐丽萍. 基于生态足迹的土地资源资产负债核算. 自然资源学报, 2022, 37(1): 149-165.

[

|

| [8] |

陈曦. 中国自然资源资产收益分配研究. 中央财经大学学报, 2019, (5): 109-120.

[

|

| [9] |

郭志京, 蒋仁开, 陈静. 论对全民所有自然资源资产行使所有权与监管权的分离. 中国土地科学, 2022, 36(12): 31-37.

[

|

| [10] |

朱道林, 张晖, 段文技, 等. 自然资源资产核算的逻辑规则与土地资源资产核算方法探讨. 中国土地科学, 2019, 33(11): 1-7.

[

|

| [11] |

卢守权, 刘晶晶. 整体性动态治理模式: 内涵、方法与逻辑框架. 中国行政管理, 2017, (3): 51-54.

[

|

| [12] |

刘超. 自然资源产权制度改革的地方实践与制度创新. 改革, 2018, (11): 77-87.

[

|

| [13] |

刘书明, 余燕. 整体性预算治理: 理论源流与实践模式: 基于预算流程重塑视角. 宏观经济研究, 2020, (9): 22-35.

[

|

| [14] |

杨志勇. 我国预算管理制度的演进轨迹: 1979—2014年. 改革, 2014, (10): 5-19.

[

|

| [15] |

孙硕, 邓淑莲. 国家治理现代化背景下的政府预算收支分类体系研究. 财政研究, 2020, (12): 22-34.

[

|

| [16] |

王雍君. 财政治理视角的支出整合、融资适配与复式预算: 一个分析框架. 财贸经济, 2021, 42(2): 5-19.

[

|

| [17] |

罗纳德·C·费雪. 州和地方财政学第二版. 吴俊培, 王莹, 毛晖, 等译. 北京: 中国人民大学出版社, 2000: 158-163.

[

|

| [18] |

范小云, 邹小备, 杨昊晰. 少儿抚养比如何影响地方政府隐性债务风险: 基于土地财政模式的研究. 南开经济研究, 2022, (5): 81-106.

[

|

| [19] |

谭荣. 全民所有自然资源资产所有权委托代理机制解析. 中国土地科学, 2022, 36(5): 1-10, 130.

[

|

| [20] |

王银梅, 陈志勇. 加强地方政府性债务预算管理的思考. 当代财经, 2016, (9): 32-42.

[

|

| [21] |

于树一. 经济新常态下发挥“四本预算”整体功能的探讨. 财贸经济, 2016, 37(10): 22-29.

[

|

| [22] |

高培勇. 论健全现代预算制度的基础工程. 中国工业经济, 2023, (1): 5-18.

[

|

| [23] |

樊丽明. 健全现代预算制度: 回顾与前瞻. 财政研究, 2022, (11): 8-13.

[

|

| [24] |

刘昆. 健全现代预算制度. 中国财政, 2022, (23): 4-7.

[

|

| [25] |

胡子航, 胡秋阳, 段文斌. 国有资本收益上缴、企业规模扩张与企业经营绩效: 对国有资本经营预算制度的评估. 南开经济研究, 2023, (2): 46-63.

[

|

| [26] |

孙玉栋, 席毓. 全覆盖预算绩效管理的内容建构和路径探讨. 中国行政管理, 2020, (2): 29-37.

[

|

| [27] |

包少卿. 国有资本经营预算与一般公共预算衔接法律制度构建问题研究. 财政科学, 2023, (3): 80-90.

[

|

| [28] |

|

| [29] |

郑涌. 深化预算绩效管理改革推进国家治理现代化. 财政研究, 2022, (11): 27-30.

[

|

| [30] |

袁月, 孙光国. 基于国家治理视角的全面预算绩效管理研究. 财经问题研究, 2019, (4): 70-76.

[

|

/

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}