全民所有自然资源资产负债表编制的思路框架

石吉金(1979- ),男,湖南株洲人,博士研究生,副研究员,研究方向为自然资源资产管理研究。E-mail: 345426385@qq.com

收稿日期: 2020-02-17

要求修回日期: 2020-04-11

网络出版日期: 2020-11-27

基金资助

国家社会科学基金项目(15AGL007)

自然资源部部门预算项目(121102000000180056)

The ideas and framework of state-owned natural resources balance sheet

Received date: 2020-02-17

Request revised date: 2020-04-11

Online published: 2020-11-27

Copyright

编制全民所有自然资源资产负债表是对我国自然资源资产负债表编制理论与方法体系的完善,也是新时期促进生态文明建设的重要举措。在理清全民所有自然资源资产负债表与自然资源资产负债表的区别和联系基础上,提出了符合用途管制和产权设置要求的自然资源资产确认方法以及自然资源保护和利用负债确认方法,初步构建了“主表+分表+基础表”的报表体系,设计出全民所有自然资源资产负债总体情况表、当期实际供应表和当期实际供应流向表三张主表。通过报表编制,反映全民所有自然资源资产家底以及占有、使用、收益、处分等各项所有权权利实现情况,以期为维护国家所有者权益、促进自然资源保护和合理利用、支撑国民经济发展提供基础信息支撑。

石吉金 , 王鹏飞 , 李娜 , 李彦华 . 全民所有自然资源资产负债表编制的思路框架[J]. 自然资源学报, 2020 , 35(9) : 2270 -2282 . DOI: 10.31497/zrzyxb.20200918

The preparation of the state-owned natural resources balance sheet is of great importance to the enrichment and improvement of the establishment theory and method system for exploration and compilation of the natural resources balance sheet in China, and it is also an important measure to promote the construction of ecological civilization in the New Era. On the basis of clarifying the differences and connections between the state-owned natural resources balance sheet and the natural resources balance sheet, this paper defines the objective of serving the unified exercise of the responsi-bilities of the state-owned natural resources assets, and proposes the natural resources asset recognition method as well as natural resource protection and utilization liability recognition method, which meet the requirements of territorial space use control and properties rights design. In addition, this paper preliminarily constructs a report system consisting of 'main tables, sub-tables, and basic tables', the three main tables of which are the summary statement of state-owned natural resources assets and liabilities, the current actual total supply statement of state-owned natural resources assets, and the current actual supply flow statement of state-owned natural resources assets. According to the preparation of state-owned natural resources balance sheet, the report table is able to reflect the situation of state-owned natural resources assets and the realization of their various ownership rights such as possession, use, income, and disposition. In the long run, the state-owned natural resources balance sheet is expected to be used for providing basic information for safeguarding national ownership rights, promoting the protection and rational use of natural resources, and supporting the development of the national economy.

Key words: state-owned assets; natural resources balance sheet; idea; framework; account system

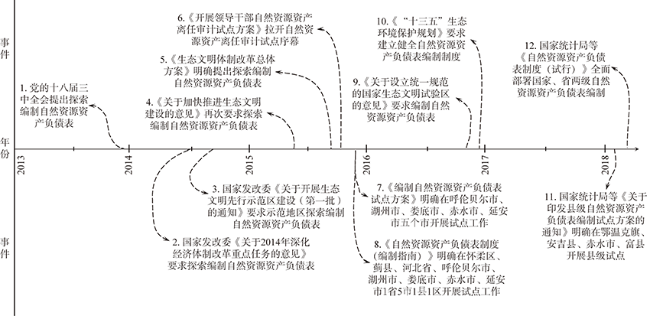

Fig. 1 The development of China's natural resources balance sheet图1 我国自然资源资产负债表发展历程 |

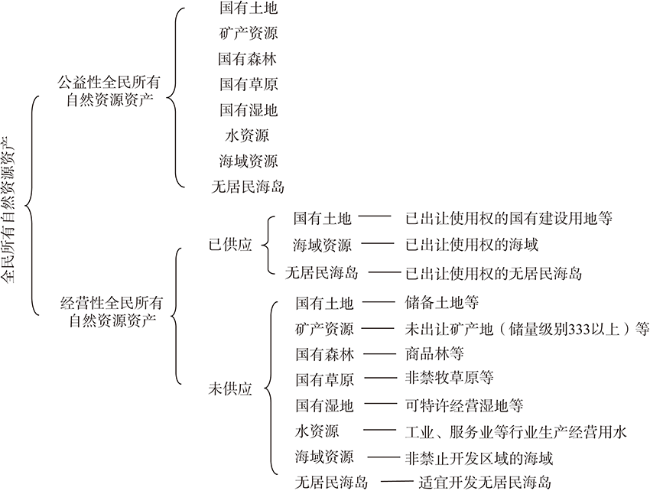

Fig. 2 The classification system of state-owned natural resources assets图2 全民所有自然资源资产分类系统 |

Table 1 Main views on natural resource liabilities表1 自然资源负债主要观点 |

| 论点 | 主要观点和内涵 | 代表学派 | 典型案例 |

|---|---|---|---|

| 有负债论 | 1. 分为资源过耗、环境损害和生态破坏三类,其中资源过耗包括自然过耗和超过各项政策红线的政策过耗;环境损害包括大气、水、土壤等环境损害;生态破坏包括森林、草原、湿地等生态系统占用和生态功能损失 | 中国科学院地理科学与资源研究所封志明等,原深圳市环境科学研究院叶有华等 | 浙江湖州市、河北承德市、福建连江县等 |

| 2. 分为应计资源耗减负债和应付环境保护负债两类,其中应计资源耗减负债指自然资源消耗所形成的负债;应付环境保护负债是人类活动导致的环境保护责任 | 中国社会科学院工业经济研究所史丹、胡文龙等 | 试编我国国家级自然资源资产负债表 | |

| 3. 界定为资源开采过耗,即自然资源实际开采使用量超过确认(或通过各种方式分配)的自然资源开采权部分 | 中国人民大学高敏雪 | 理论研究 | |

| 4. 界定为自然资源数量和质量现状与管理目标间的差额 | 北京林业大学张卫民等 | 理论研究 | |

| 5. 反映环境成本,通过核算“资源耗损价值、环境退化价值、资源管理支出与环境保护支出”等账户的实物与价值量来计量 | 中国自然资源经济研究院姚霖、余振国 | 理论研究 | |

| 6. 包括应付污染治理成本、应付超载补偿成本、应付生态恢复成本、应付生态维护成本四部分 | 武汉理工大学张友棠等 | 理论研究 | |

| 7. 包括破坏修复成本、生态恢复成本、自然资源维护成本、生态补偿四部分 | 广东中山市环保局杜敏等 | 广东中山市五桂山 | |

| 无负债论 | 1. 编制自然资源资产数量、质量等统计表,不显示自然资源负债 | 国家统计局等部门及部分试点地区 | 湖北鄂州、山东淄博等部分试点地区 |

| 2. 根据负债的定义和SEEA2012现行规定,编制平衡表,不确认自然资源负债 | 中国人民大学耿建新等 | 宁夏永宁等 |

Fig. 3 The classification system of state-owned natural resource liabilities图3 全民所有自然资源负债分类系统 |

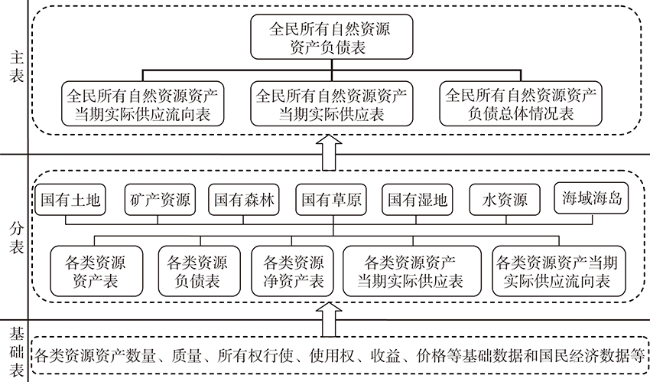

Fig. 4 The account system of state-owned natural resources balance sheet图4 全民所有自然资源资产债表报表体系 |

Table 2 The summary statement of state-owned natural resources assets and liabilities (亿元)表2 全民所有自然资源资产负债总体情况表 |

| 自然资源资产类别 | 自然资源部直接 行使所有权 | 委托中央其他部门 代理行使所有权 | 委托地方政府代理 行使所有权 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 资产 | 负债 | 净资产 | 资产 | 负债 | 净资产 | 资产 | 负债 | 净资产 | |||

| 一、公益性全民所有 自然资源资产 | |||||||||||

| 1. 国有土地 | |||||||||||

| 期初存量 | |||||||||||

| 期末存量 | |||||||||||

| …… | |||||||||||

| 小计 | |||||||||||

| 二、经营性全民所有 自然资源资产 | |||||||||||

| 1. 已供应 | |||||||||||

| (1)国有土地 | |||||||||||

| 期初存量 | |||||||||||

| 期末存量 | |||||||||||

| …… | |||||||||||

| 2. 未供应 | |||||||||||

| (1)国有土地 | |||||||||||

| 期初存量 | |||||||||||

| 期末存量 | |||||||||||

| …… | |||||||||||

| 小计 | |||||||||||

| 合计 | |||||||||||

Table 3 The current actual total supply statement of state-owned natural resources assets表3 全民所有自然资源资产当期实际供应表 |

| 自然资源资产类型 | 自然资源部直接 行使所有权 | 委托中央其他部门 代理行使所有权 | 委托地方政府代理 行使所有权 |

|---|---|---|---|

| 一、公益性全民所有自然资源资产 | |||

| 1. 国有土地 | |||

| 当期实际供应/hm2 | |||

| 当期利用收入/万元 | |||

| …… | |||

| 当期利用收入小计/万元 | |||

| 二、经营性全民所有自然资源资产 | |||

| 1. 国有土地 | |||

| (1)国有建设用地 | |||

| 当期供应指标/hm2 | |||

| 当期实际供应/hm2 | |||

| 其中:出让 | |||

| 面积/hm2 | |||

| 成交价款/万元 | |||

| …… | |||

| 当期供应收入小计/万元 | |||

| 当期供应收入合计/万元 |

Table 4 The current actual supply flow statement of state-owned natural resources assets (hm2)表4 全民所有自然资源资产当期实际供应流向表 |

| 所有权 具体行使主体 | 资产类型 | 国民经济行业 | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 农、林、牧、渔业 | 采矿业 | 制造业 | 电力、热力、燃气及水生产和供应业 | 建筑业 | 批发和零售业 | 交通运输、仓储和邮政业 | 住宿和餐饮业 | 信息传输、软件和信息技术服务业 | 金融业 | 房地产业 | 租赁和商务服务业 | 科学 研究和技术服务业 | 水利、环境和公共设施 管理业 | 居民服务、修理和其他服务业 | 教育 | 卫生和社会 工作 | 文化、体育和娱乐业 | 公共管理、社会保障和社会组织 | ||

| 自然资源部直接行使所有权 | 一、公益性全民所有自然资源资产 | |||||||||||||||||||

| 1. 国有土地 | ||||||||||||||||||||

| …… | ||||||||||||||||||||

| 二、经营性全民所有自然资源资产 | ||||||||||||||||||||

| 1. 国有土地 | ||||||||||||||||||||

| …… | ||||||||||||||||||||

| 委托中央其他部门代理行使所有权 | 一、公益性全民所有自然资源资产 | |||||||||||||||||||

| 1. 国有土地 | ||||||||||||||||||||

| …… | ||||||||||||||||||||

| 二、经营性全民所有自然资源资产 | ||||||||||||||||||||

| 1. 国有土地 | ||||||||||||||||||||

| …… | ||||||||||||||||||||

| 委托地方政府代理行使所 有权 | 一、公益性全民所有自然资源资产 | |||||||||||||||||||

| 1. 国有土地 | ||||||||||||||||||||

| …… | ||||||||||||||||||||

| 二、经营性全民所有自然资源资产 | ||||||||||||||||||||

| 1. 国有土地 | ||||||||||||||||||||

| …… | ||||||||||||||||||||

| [1] |

[

|

| [2] |

[

|

| [3] |

[

|

| [4] |

[

|

| [5] |

[

|

| [6] |

[

|

| [7] |

[

|

| [8] |

[

|

| [9] |

[

|

| [10] |

[

|

| [11] |

[

|

| [12] |

[

|

| [13] |

[

|

| [14] |

[

|

| [15] |

[

|

| [16] |

[

|

| [17] |

[

|

| [18] |

中共中央. 《中共中央关于全面深化改革若干重大问题的决定》辅导读本. 北京: 人民出版社, 2013: 350-351.

[The Central Committee of the Communist Party of China. Guidance Reading of Decision of the Central Committee of the Communist Party of China on Some Major Issues Concerning Comprehensively Deepening the Reform. Beijing: People's Publishing House, 2013: 350-351.]

|

| [19] |

[

|

| [20] |

[

|

| [21] |

[

|

| [22] |

[

|

/

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}